|

| The benefits of foreign investment in housing flow through the rest of the economy. |

It would be both sad and funny if Australia rejected a renewable, $10 billion-a-year, foreign-exchange-earning, non-outsource-able, employment-rich business opportunity just because a mixture of xenophobes and myopic protectionists collectively chanted: "I don't like it."

It would be sad because of the quality local employment opportunities foregone and because the nation would miss a chance to be richer in several senses of the word.

“Struggling treasurers around the nation drool at the thought of those cashed-up Chinese.”

It would be funny, in a perverted sort of way, because many of the people chanting against foreigners buying Australian housing – something we're obviously better than anyone else at providing – also bewail the demise of protected industries that we've proven to be not so good at.

World beaters

No one does Australian real estate better than Australia, but it turns out half the world is better at building cars. It's a no-brainer.

Paul Sheehan's "Cashed-up Chinese" story on these pages summarised many of anecdotal reservations about an alleged Asian invasion of the domestic housing market, while Saturday's Chinese buyers story suggested a generation of Australians were being priced out of $5-million-plus Bellevue Hill real estate. Very droll.

There is a bigger point though about the opportunity provided by foreigners wanting to buy housing here and the way markets work. The good ol' laws of supply and demand still apply, meaning movements by either of those variables affect price.

The central complaint seems to be that extra demand from foreign buyers (and Keane points out that such buying actually fell in 2012-13) is making it harder for the minority of Australians who compete with those foreigners in the market.

And it is a fairly small minority. Roughly two-thirds of Australians either own their homes outright or are paying them off, so they benefit from housing prices rising, while a fair whack of the remaining third either don't want to buy a property or have such low income as to not have prospects of buying in last year's market, never mind the present one.

So this is essentially a protectionist argument – part of the market wants to reduce the competition. And like all protectionism, it would be at a substantial cost to the rest of the economy.

Supply problems

But demand is only half the story. If there is a problem with price, it's the failure of all three levels of government that our supply of housing is not more elastic, not quicker to respond to a surge in demand.

respond to a surge in demand.

Interminable state planning delays, NIMBY-dominated local councils, various damaging taxes and the always-growing thicket of red and green tape conspire to make housing more expensive and harder for developers to respond to demand.

Despite the many official impediments, the market mechanism struggles on. After under-building for a decade, improved demand lifts prices enough to provide incentives for developers to increase supply. It would be nice if governments helped the process instead of hindering it, but the cycle rolls on anyway.

As Reserve Bank governor Glenn Stevens reminded the House of Representatives economics committee on Friday, prices rise and fall:

"Credit to households for investment in housing is (growing by) eight or nine per cent a year. I would say that is probably fast enough. I repeat what I have said before that in Sydney in particular - but not just Sydney now - there has been a very big run up in investor activity. That is okay, but people need to keep in mind that prices do not just rise; they can fall and have fallen."

In the meantime, greater investor activity is effectively lowering rents – it's that supply and demand thing again. When not bleeding for would-be first home buyers (FHBs), the usual suspects are concerned about the cost of rental accommodation as that is one of the two markets where the genuinely less-advantaged people live.

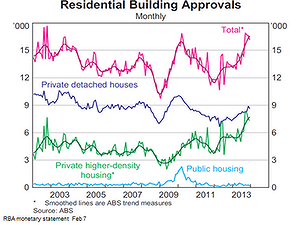

Public housing

The other is public housing, which is reason to point to the first of two RBA graphs. As can be immediately seen, there's stuff-all happening in the public housing sector, in keeping with the overall government proportion of investment in this country running at its lowest level in at least a half a century and probably much, much longer.

Aside from a GFC-stimulus-related surge in 2009-10, public housing approvals are going nowhere.

The way would be open for brave and visionary governments to develop a stock of public housing that could be bought and sold to smooth the housing cycle – but first it would be necessary to find a brave and visionary government. None is in prospect.

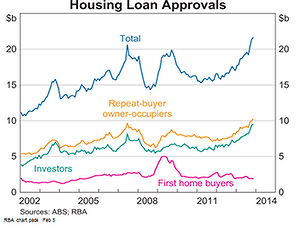

Another RBA graph tells us something else about the disproportionately-publicised first home buyer element: in absolute terms, it's more flat than shrinking.

Yes, the proportion of FHBs is at a low, but that's more about the rest of the market taking off as FHBs falling.

Aside from the distortion and pull-forward created by the federal and state GFC stimulus incentives, FHB activity has been fairly steady.

And it's simply stating the bleeding obvious that, with housing prices mostly rising rather than falling, it's nearly always the case that FHBs have never had to borrow and pay more to enter the market.

In any event, it gets back to the supply thing where FHBs problems are best addressed, rather than trying to restrict demand.

Bigger picture

Meanwhile, an appreciation of how good Chinese buyers are for the broader economy is missed.

Using Bernard Keane's most generous case figure, an over-stated $10 billion a year, that is an amazing amount of employment creation that goes way beyond the tradies.

The preponderance of new housing in Chinese purchases means the wealth does indeed get spread around.

New housing likes new appliances and floor coverings, so retailers get a feed. And as the RBA has mentioned, a significant part of the Australian manufacturing industry is housing-related. The lift in housing starts is doing a wonderful job in all sorts of jobs.

As for the evil business of state government stamp duties and fees on property, struggling treasurers around the nation drool at the thought of those cashed-up Chinese.

And there's the truism that foreign buyers can't take their real estate purchases home.

What they build stays here, adding to housing stock that needs adding to. As previously reported, we're on track to add another 2.3 million people over the next five years. At present, we're arguably still in catch-up mode from under-building. Without the stimulus of investors to get the country building now, we'll face demand-induced price pressure all of our own soon enough.

National renewal

The yet-bigger picture is less tangible – the renewal that each generation of fresh blood brings to the nation, the fire in the belly of people with fresh eyes seeing the opportunities available here for investors and workers. That's the very best kind of foreign investment here, the enriching human capital. The RBA's Glenn Stevens certainly didn't sound worried about it on Friday:

"In particular parts of our cities, including where we are sitting right now [Sydney CBD], the role of foreign investors is quite prominent indeed. I suspect it is rather less prominent around most of the metropolitan areas than some of the headlines might suggest; nonetheless, there is a role.

"As a country we tend to feel that we should be open to foreign investment - we generally like that. This is a form of that, just as foreign investors buying shares in listed companies or doing direct investment in resource projects or whatever it might be is a form of it. It has its effect on asset values and the exchange rate, just like all the other forms of foreign investment. I suppose the question is really: how big a problem do you really think it is?

"Foreign investors are generally confined to buying new structures. That is where it is easiest for them to come in. It cannot be beyond our capacity over time to meet that demand and to meet the legitimate demands of our own citizens for structures as well, can it? If we cannot do that, if there is a supply side constraint, I would say that is an issue worth addressing in its own right.

"Beyond that, it probably goes to broader questions of how welcoming we wish to be to foreign investment generally. That can be a vexed issue at times. With all due respect, that is a matter for our parliament to manage."

Memo our parliament: try the vision thing and keep an eye on the big picture, not the pockets of highly visible by myopic protectionists.

TheSydenyMorningHerald BusinessDay

Please

contact us in case of Copyright Infringement of the photo sourced from the internet, we will remove it within 24 hours.

京公网安备 11010502030593号

京公网安备 11010502030593号